- November 26, 2022

- Posted by: Gavtax gavtax

- Category: SMALL BUSINESS TAXES

An Installment Sale as the name suggests is a sale of property where the sale price is paid in installments and at least one payment is received after the tax year of the sale.

Using this method, a taxpayer can avoid paying the entire gain in the year of sale.

You cannot use the installment sale to report a loss.

Example: In 2019, you sold the land for $100,000. You received a $20,000 down payment and a buyer’s note for $80,000. The note mentions that there are four annual payments of $20,000 each, plus 8% interest, beginning in 2020. This is a classic example.

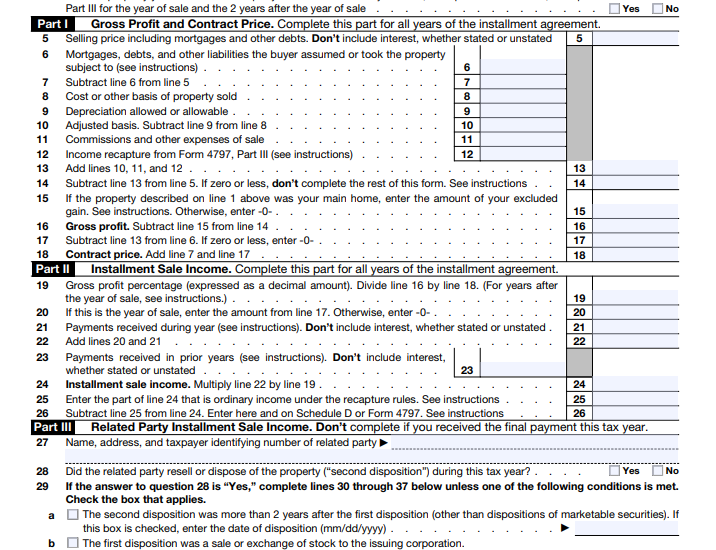

How to Report an Installment Sale?

Most likely, you will use Form 6252 to report installment sale income from casual sales of real or personal property during the tax year.

Installment sale income might also be reported on Schedule D (Form 1040), Form 4797, or both.

If the property was your main home, you may be able to exclude part or all of the gain (under the primary home sale exclusion rule).

Useful Tips:

- Dealer sales or people who are in the business of buying and selling properties do not qualify for installment sales. However, the rule does not apply to an installment sale of property used or produced in farming.

- Stocks and Securities are also not eligible for installment sales.

- The sale of inventory of personal property doesn’t qualify as an installment sale even if you receive a payment after the year of sale.

- Fair market value (FMV). This is the price at which property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having a reasonable knowledge of all the necessary facts. ( source: IRS)

Read Also: